What credit score is needed to buy a house? What types of loans are available to you? Find out the answers to these burning questions, here.

After years of growth in housing prices, the real estate market is beginning to cool down. As a matter of fact, in some of the country’s biggest cities, price growth has dropped by close to 3%.

With the market becoming increasingly favorable to home buyers, more and more people are asking the question, “What credit score is needed to buy a house”.

Unfortunately, that’s a loaded question.

Because of its intricacies, we’ve decided to dedicate a whole article to breaking down the basics of mortgage’s relation to credit, what kind of credit you’ll need to get a home, and how to get a home if your credit score is below average.

What Is a Mortgage and What Does It Have to Do With Credit?

When people ask, “What credit score is needed to buy a house?” they’re really asking “What credit score is needed to get a mortgage?”.

For the uninitiated, a mortgage is a product offered to home buyers by lenders.

Since most home buyers can’t buy their house all-cash, they turn to lenders to purchase the home for them. Buyers then make payments to lenders over the course of 15-30 years.

This process encompasses what a mortgage is.

The problem with mortgages for lenders is that they need to trust people to pay them back hundreds of thousands of dollars.

What if the home buyer doesn’t make those payments? The lender would be stuck with a house they have no use for.

In order to prevent that from happening, lenders screen buyers using their credit score.

A buyer with a high credit score represents a low risk of defaulting on payments to lenders. That means lenders are more eager to do business with them and will offer them better interest rates.

Buyers with low credit score represent a high risk of default. This can lead to lenders increasing interest rates or the outright rejecting buyers.

What Is the Lowest Credit Score You Can Have to Get Approved for a Mortgage?

The question of “what the lowest acceptable credit score is to get a mortgage” doesn’t have a solid answer when looking at your broad options.

At the end of the day, any private lender can approve a mortgage for any buyer no matter their credit score. There is no legal lower limit.

For example, if you were to come to a lender with a low credit score but had proof of substantial income and had a sizable down payment available, there is a good chance you would get approved for a mortgage.

At the end of the day, most lenders will take your complete financial picture into consideration, weigh your risk, and decide on a case-by-case basis whether or not to work with you.

The only instance in which there is a stated lower credit limit on mortgages is when taking out an FHA loan.

FHA loans are government backed, require low down payments, and state that you need at least a 580 credit score to qualify for a 3.5% down payment. Alternatively, you could have a 500 credit score and qualify for a 10% down payment.

What is the Average Credit Score Mortgage Applicants Carry?

Since a lower limit on credit scores is hard to define with mortgages, a better way to figure out where you measure up is to look at averages.

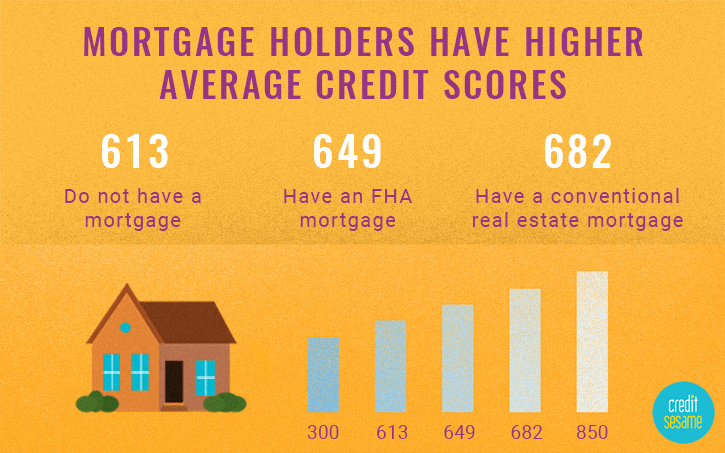

Every lender has their own (often hidden) average when it comes to mortgage approvals. Credit score aggregator “Credit Sesame” has a helpful infographic which sheds some light on what its data has concluded.

Per the infographic, for FHA mortgages, the average borrower has a 649 credit score. For non-FHA mortgages, the average borrower has a 682 credit score.

How to Purchase a Home With Bad Credit

If the answer to “What credit score is needed to buy a house?” we’ve provided isn’t what you wanted to hear, know that you can still buy a home despite having below-average credit.

To improve your odds of approval, consider doing the following.

Get a Co-Signer

A co-signer is someone with good credit who will take on your loan with you. Having a co-signer vouch for you will substantially increase your odds of approval.

Opt for an FHA Loan

FHA loans are a lot less strict when it comes to approving loan applicants. If you have low credit, keep your search strictly to FHA products.

Put Down a Higher Down Payment

If your credit is bad, another way you can assure lenders you’re good for the money is by putting down a substantial down payment. The higher your down payment, the better your odds are of approval.

Work to Improve Your Credit

At the end of the day, the better your credit is, the cheaper your mortgage product will be. That’s why it’s recommended that rather than trying to work around your bad credit, you work to improve it.

Even a year of credit repair attention can boost your score enough to save thousands when seeking a home loan.

You can start improving your credit by consolidating debt through microloans or microcreditos.

Wrapping Up What Credit Score is Needed to Buy a House

We hope that by this point you understand all of the ins and outs of what credit score is needed to buy a house.

Use what you’ve learned to put your unique financial situation into context and put into motion a realistic strategy for your home purchase!

For more info on all things real estate and more, check out azbigmedia.com.

{kind=link}