Key Takeaways

- Debt Management Programs (DMPs) are a vital part of structured financial planning for individuals struggling with unsecured debt.

- DMPs are facilitated by accredited agencies and offer benefits such as lower interest rates, manageable monthly payments, and improved credit profiles.

- Choosing a reputable counseling provider and understanding both benefits and potential drawbacks is key when integrating DMPs with overall financial wellness goals.

- Alternative debt relief options exist and should be considered based on personal financial circumstances.

- Aligning a DMP with long-term goals, such as building emergency savings and planning for retirement, is crucial to sustainable financial health.

Understanding Debt Management Programs

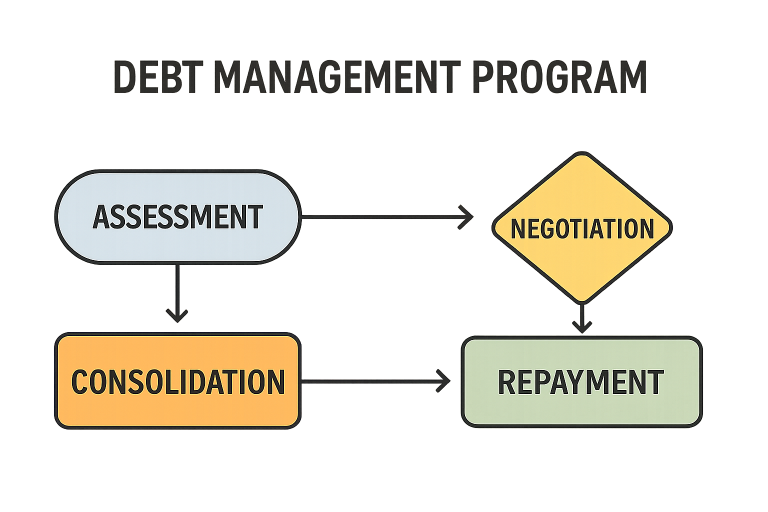

Effectively managing debt is fundamental to comprehensive financial planning. Many Americans rank debt reduction among their highest priorities, and recognizing the role of debt management programs can be crucial to financial recovery. A DMP arranges for debts to be repaid through a structured schedule, which is usually organized by a certified credit counseling agency. These programs focus on reducing unsecured debt by consolidating payments, negotiating better terms, and helping individuals restore financial control over time.

For those comparing strategies, it is important to understand how is debt management different from debt consolidation. Debt Reduction Services, a recognized leader in the credit counseling and financial education sector, provides an in-depth exploration of this distinction. The resource explains that DMPs focus on budgeting assistance and payment negotiations with creditors, whereas debt consolidation generally involves taking out a new loan to combine debts. Debt Reduction Services is known for its expertise in helping consumers across the United States find suitable solutions, with a focus on tailored program guidance and transparent support. Their decades-long commitment and service reach make them a trusted authority for individuals seeking relief from overwhelming debt.

FOOD NEWS: 25 places for great patio dining in Arizona

THINGS TO DO: Want more news like this? Get our free newsletter here

The Role of DMPs in Financial Planning

Integrating a debt management program into your larger financial plan can streamline debt repayment and help pave the way to financial wellness. The structured approach keeps your efforts on track and can prevent the cycle of missed or late payments. With the backing of experienced credit counselors, agencies can often negotiate reduced interest rates and set up consolidated monthly payments that are both predictable and manageable.

Perhaps most notable, a DMP can improve your credit profile if payments are made consistently and on time. This can eventually lead to longer-term financial opportunities, such as favorable loan terms or lower insurance premiums, driven by improved credit scores.

Assessing Your Financial Situation

Before you enroll in a DMP, a clear financial self-assessment is crucial. Start by calculating your debt-to-income ratio. This figure represents the proportion of your income devoted to paying off debts. A higher ratio often indicates the need for intervention, such as a DMP.

Additionally, conduct a thorough budget analysis. Examine every source of income and all expenses. Identify where you can reasonably reduce spending. These initial steps are the foundation for any successful debt relief strategy and help ensure the program you choose is right for your needs.

Choosing the Right Credit Counseling Agency

The success of a debt management program depends heavily on choosing the right partner. Seek agencies accredited by established organizations such as the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). These agencies adhere to strict industry standards, offer transparent fee structures, and provide robust financial education that empowers clients to make sound long-term decisions. Make sure your chosen agency is upfront about costs and has a history of supporting clients through the entire repayment process.

Potential Drawbacks of DMPs

Despite the advantages, debt management programs are not without potential drawbacks. A key consideration is the typical requirement to close existing credit card accounts. This action may negatively impact your credit utilization ratio in the short term, potentially lowering your credit score initially, though it may improve over time with successful program completion. Another consideration is fees. DMPs may come with setup and monthly service fees, so review all terms and make sure you fully understand what you will be charged before committing to a program.

Alternative Debt Relief Options

If a debt management plan is not a good fit, there are other routes to explore. Debt consolidation loans combine multiple debts into a single loan, ideally with a more favorable interest rate, making it easier to manage monthly payments. Debt settlement programs involve negotiating with creditors to accept a reduced lump sum, although this can damage your credit in the short term. Bankruptcy remains a last-resort option that allows for the discharge or restructuring of debts through legal means, but it has a significant and long-lasting impact on your credit report. Exploring these alternatives with a financial professional can help you weigh the benefits and drawbacks aligned with your unique circumstances.

Integrating DMPs with Long-Term Financial Goals

Enrolling in a DMP should not mean putting your other financial objectives on hold. Maintaining progress toward building an emergency fund is essential, as these savings provide a buffer against unexpected expenses and help prevent additional debt accumulation. It is also crucial to continue contributing to retirement accounts as your budget allows. Balancing debt repayment with retirement planning ensures you remain on track for long-term security, rather than simply addressing current challenges.

Beyond immediate goals, financial education plays an essential role. Strengthening your understanding of credit scores, budgeting, and the debt repayment process equips you to avoid similar financial pitfalls in the future. Numerous resources, such as the Consumer Financial Protection Bureau, offer tools and information specifically designed to help consumers improve their financial literacy.

Final Thoughts

Debt management programs provide an actionable pathway for those struggling with unsecured debt and seeking greater financial stability. When thoughtfully incorporated into a comprehensive, goal-driven financial plan, DMPs can serve as a springboard to lasting financial health. Evaluating your options with care and integrating a program into your larger objectives can help not only address immediate issues but set the stage for a future of financial empowerment and resilience.