Dreaming of soft sand, Gulf breezes, and no state income tax? You’re not alone. Florida’s population topped 23 million last year, and newcomers keep arriving. But paradise can get pricey. Homeowners insurance now averages $7,136—nearly triple the national mark. Add hurricane deductibles, Medicare surcharges, and quirky property-tax caps, and a beach retirement quickly grows complex.

That’s why planning matters. We sifted through SEC filings, fee schedules, and Florida-specific expertise to find the fiduciary advisers we’d trust with our own move.

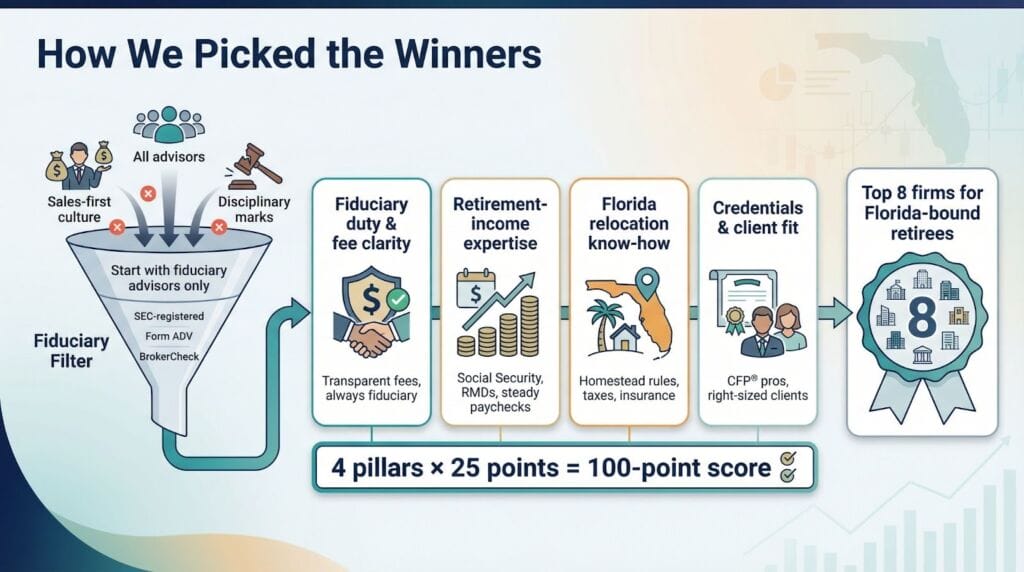

How we picked the winners

You trust a planner with life savings you spent decades building, and we took that responsibility seriously.

We built a clean pool: only SEC-registered advisers acting as fiduciaries all the time. We cross-checked each firm’s Form ADV and FINRA BrokerCheck records for disciplinary marks, then scored survivors on four weighted pillars:

- Fiduciary duty and fee clarity

- Depth of retirement-income expertise

- Florida relocation know-how

- Team credentials and client fit

Each pillar carried 25 possible points for a perfect 100. We examined hard evidence: fee schedules, CFP® headcount, office footprints, and documented services such as Social Security timing or homestead-exemption guidance. Three firms stood out.

3. Certified Financial Group: forty-five years of “certified” confidence

When a firm has guided clients through oil embargoes, dot-com frenzies, and three bear markets, you listen. Certified Financial Group (CFG) opened near Orlando in 1976 and still leans on the same core promise: every planner holds the CERTIFIED FINANCIAL PLANNER™ mark and signs a fiduciary oath before meeting a client.

Twelve CFP® professionals serve about 1,800 families, giving each household a small-team feel inside a mid-sized practice. Longevity matters: many advisers have spent two decades under the same roof, so you are not re-explaining your goals every few years.

Education sits at the firm’s heart. CFG’s founders launched a live call-in radio show, “On The Money,” in 1984 and still air it weekly. Tune in for Social Security timing tips, Medicare cost updates, and candid talk about annuities. Free monthly workshops extend that classroom spirit to retirees who prefer in-person learning.

Plans start with a flat-fee engagement, ideal if you only need a roadmap before handling investments yourself. Ongoing management runs about 1 percent of assets, stepping down for larger balances. CFG excels at nuts-and-bolts retirement mechanics: pension-versus-lump-sum math, Roth-conversion windows, and required-minimum-distribution timing. Shift those decisions into a Florida context—with higher homeowner insurance and tricky homestead rules—and the firm’s 45-year playbook becomes a practical safety net.

2. FirsTrust: fee-only advice for every Florida zip code

FirsTrust guards its independence. The employee-owned firm rejects commissions, revenue sharing, and soft-dollar perks, and puts that pledge in writing for every client.

Five offices ring the state from Daytona Beach to Sarasota, giving you local insight whether you land in the Panhandle or Palm Beach. That footprint delivers practical intel: which counties process homestead filings fastest, how flood-zone maps alter insurance quotes, and where a newcomer can find a primary-care doctor who accepts Medicare.

Planning unfolds in three steps. The Build phase maximizes pre-retirement savings and trims taxes. Retire-Ready starts five years before your last paycheck, easing portfolio risk and lining up Social Security timing. The final Income phase manages withdrawals, Medicare, and estate adjustments so money lasts and heirs stay protected.

Most clients arrive with $1 million or more, yet FirsTrust offers flat-fee plans for motivated savers below that mark. Asset-management fees begin at 1 percent and fall on larger balances.

1. Signature Financial Solutions: your one-stop retirement paycheck

Some advisers juggle investments while others sell insurance, leaving you to stitch the pieces together. Signature Financial Solutions (SFS) in Tampa removes that hassle by housing every retirement-income tool under one roof and pairing it with a written fiduciary pledge.

The process starts with one question: “How large a paycheck do you need when work stops?” Advisers feed your answer into the firm’s proprietary NextPhase model, stress-test it for market drops, inflation spikes, and long-term-care costs, then craft a year-by-year withdrawal plan designed to last 30 years or more. Unsure if your current nest egg is enough? Plug the numbers into SFS’s free retirement savings calculator to see your projected balance and how extra monthly contributions could compound before you even schedule a meeting.

SFS is fee-based and independent, so it can manage both sides of the ledger: low-cost portfolios for growth and, when helpful, commissionable products such as long-term-care insurance. The rule is simple: if an annuity or policy will not raise net income or lower risk, the team says no.

No strict minimums keep mid-career savers out. Clients with $300,000 can access the same tools as millionaires, and bilingual planners welcome Florida’s growing Spanish-speaking retiree base. SFS tops our list because it tackles the toughest task: turning lifelong savings into a steady, predictable paycheck so you can watch sunsets, not spreadsheets.

How to choose a planner for your Florida move

- Start with fiduciary proof. Ask directly, “Will you sign a fiduciary oath that binds you at all times?”

- Zoom in on relocation skill. Probe for concrete examples: “Walk me through how you helped a recent client establish domicile and file the Save Our Homes cap.”

- Clarify the fee math. You should hear something like, “Our tiered schedule starts at 1 percent on the first $1 million, then drops.”

- Check the background. Five minutes on SEC Adviser Search and FINRA BrokerCheck can save years of regret. Zero disciplinary marks is the baseline.

Follow these steps, and the Sunshine State’s financial quirks become just another line item on a well-built plan.