June posted month-over-month increases in home sales (up 5.4% from May) and inventory (up 7.2%) while year-over-year activity continued to trail the strong results of early 2022. June 2023 home sales were 18.7% below last June’s, contributing to a first-half 24% decline in closings compared to the first half of 2022 across the 52 metro areas surveyed in the RE/MAX National Housing Report. Of note: Phoenix leads the U.S. with the biggest percentage decrease in new home listings.

LEARN MORE: Housing affordability rises across all Arizona metros

June’s year-over-year decrease in new home listings of 10.7% was the first such decrease in the past 13 months. New listings, although down 25% compared to a year ago, were up 0.5% over May.

Typically the biggest month for home sales, June produced a median sales price of $425,000 which was the highest since June 2022’s peak price of $426,000.

“June’s month-over-month gain in sales is largely seasonal, but it shows the market’s resiliency in the face of low inventory and higher interest rates,” said RE/MAX President and CEO Nick Bailey. “While we probably won’t see a significant jump in sales activity in the short term, demand is strong and houses are selling when they’re priced right. The expertise of an experienced real estate agent continues to be an important part of the equation for buyers and sellers navigating this rebalancing market.”

Shelley Bridge of RE/MAX Cherry Creek in Denver, CO agreed. “We are back to a more normal market. Homes that are in good locations, good condition and priced fairly are still selling quickly and with multiple offers. However, properties that don’t meet these criteria are taking longer to sell and often need to have price reductions in order to attract a buyer.”

Other notable metrics:

- Months’ Supply of Inventory in June was 1.4, up from May’s 1.3 but below the 1.6 months recorded a year ago.

- The average close-to-list price ratio for June was 100%, indicating that homes sold for the asking price on average. This matched May’s ratio and was a decline from the 102% ratio recorded a year ago.

- Homes sold in June were on the market for an average of 31 days, which was the same in May but 9 days longer than June of last year.

Highlights and local market metrics for June include:

New Listings : Of the 52 metro areas surveyed in June 2023, the number of newly listed homes was up 0.5% compared to May 2023, and down 25.0% compared to June 2022. The markets with the biggest decrease in new home listings were Phoenix, AZ at -54.4%, Las Vegas, NV at -43.3% and Seattle, WA at -35.9%. No markets had an increase in year-over-year new listings percentage.

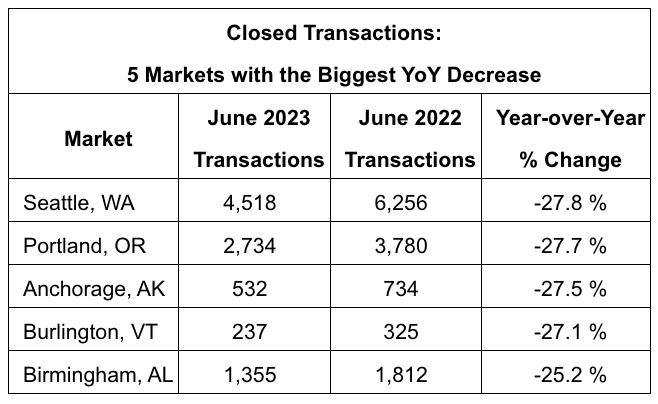

Closed Transactions: Of the 52 metro areas surveyed in June 2023, the overall number of home sales was up 5.4% compared to May 2023, and down 18.7% compared to June 2022. The markets with the biggest decrease in year-over-year sales percentage were Seattle, WA at -27.8%, Portland, OR at -27.7%, and Anchorage, AK at -27.5%. Only one metro area had a year-over-year sales percentage increase in June, Coeur d’Alene, ID at +0.9%.

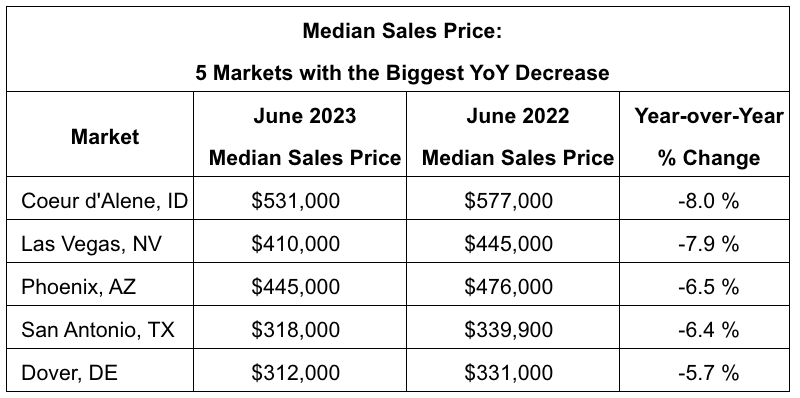

Median Sales Price – Median of 52 metro area prices: In June 2023, the median of all 52 metro area sales prices was $425,000, up 2.4% compared to May 2023, and down 0.3% from June 2022. The markets with the biggest year-over-year decrease in median sales price were Coeur d’Alene, ID at -8.0%, Las Vegas, NV at -7.9%, and Phoenix, AZ at -6.5%. The markets with the biggest year-over-year increase in median sales price were Trenton, NJ at +11.5%, Omaha, NE at +10.2%, and Anchorage, AK at +7.8%.

Close-to-List Price Ratio – Average of 52 metro area prices: In June 2023, the average close-to-list price ratio of all 52 metro areas in the report was 100%, flat compared to May 2023, and down from 102% compared to June 2022. The close-to-list price ratio is calculated by the average value of the sales price divided by the list price for each transaction. When the number is above 100%, the home closed for more than the list price. If it’s less than 100%, the home sold for less than the list price. The metro areas with the lowest close-to-list price ratio were Miami, FL at 95%, followed by a tie between Coeur d’Alene, ID and New Orleans, LA at 97%. The highest close-to-list price ratios were Hartford, CT at 106%, followed by a three-way tie between Manchester, NH, San Francisco, CA, and Trenton, NJ at 104%.

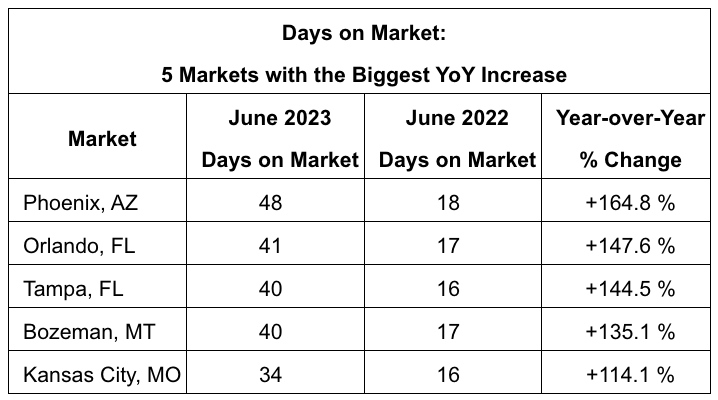

Days on Market – Average of 52 metro areas: The average days on market for homes sold in June 2023 was 31, flat compared to the average in May 2023, and up 9 days from the average in June 2022. The metro areas with the lowest days on market were a tie between Baltimore, MD and Washington, DC at 11, followed by Manchester, NH at 12. The highest days on market averages were in Fayetteville, AR at 77, Coeur d’Alene, ID at 57, followed by a tie between Miami, FL and San Antonio, TX at 51. Days on market is the number of days between when a home is first listed in an MLS and a sales contract is signed.

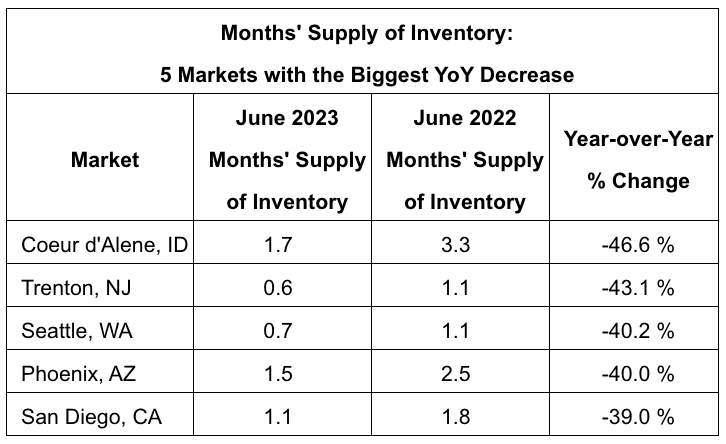

Months’ Supply of Inventory – Average of 52 metro areas: The number of homes for sale in June 2023 was up 7.2% from May 2023 and down 10.7% from June 2022. Based on the rate of home sales in June 2023, the months’ supply of inventory was 1.4, up from 1.3 in May 2023, and decreased compared to 1.6 in June 2022. In June 2023, the markets with the lowest months’ supply of inventory were a three-way tie between Charlotte, NC, Manchester, NH, and Trenton, NJ at 0.6. The markets with the highest months’ supply of inventory were Bozeman, MT at 3.0, San Antonio, TX at 2.9, and Houston, TX at 2.8.